Eve is here. Thomas Neuberger delves into the question of what happens to U.S. real estate prices, which always seem to be on the rise, if you run into the problem of non-existent or extremely expensive insurance.

Written by Thomas Neuberger. It was first published in god's spy

On Friday, November 9, 2018, the Woolsey Fire destroys a home near Lake Malibu in Malibu, California. AP Photo/Ringo HW Chiu

If the flow of this man-made water somehow stopped, California's economy, which was worth about $1 trillion at the start of the new millennium, would collapse like a neutron star.

—Mark Laisner dangerous place,Quote here

Insurance is related to life

Much of First World life and its stability is built around insurance.

We already know how much hell people without health insurance go through. What is that crisis? to us now, It has been At least in the United States, no one in power dares to address this issue.

The donor class, especially the queens and kings of medicine, will turn a blind eye to the powerful donors and force them to live in the wilderness, perhaps in Kentucky. Or the main. (When I say power, I don't mean Bernie Sanders. He's not the decision maker. I mean Joe Biden and the people at the helm of Congress.)

But more than our health depends on proper insurance. Our homes are also shelters that allow us to live. forest and tenement house and tipi; something to keep most of us live in citiesIn other words, it depends on your ability to prevent destruction.

Now, imagine you lived in a state where home and property insurance was not available. what would you do? I think most people move to another state. The rest of the population is left uninsured and evacuated to the spot.

Could that result be possible? Let's take a look.

uninsured person day

The day when the entire state will be uninsured is approaching. Many people choose wildfire-prone California as an early choice, and for good reason.

A structure and motorcycle catch fire at an RV park during the Woolsey Fire in Malibu, California, November 10, 2018.Kyle Grillot/Washington Post/Getty Images

But California is big and varied, so some disasters have to pile up there. water shortagelarge fires, especially in places where wealthy people live, like Malibu Canyon; earthquake. Collapse of the water table. Moreover, before the state becomes uninhabitable. It will happen, but maybe not right away.

Florida is a different story.There Typhoon Haiyan–-type events can wipe out coastal and inland properties in a single day, rendering remaining properties uninsurable.

Image courtesy of the U.S. Naval Institute Government forecasters said Thursday that Typhoon Haiyan, with winds of 225 kph (140 mph) and gusts as high as 260 kph (162 mph), was expected to hit Eastern Samar in the eastern Philippines on Friday. He said it was possible that the force would increase before directly hitting the state. AP Photo/U.S. Naval Research Institute

That day could be tomorrow, or it could be any day you like. Atlantic hurricane season runs from June to November, but hurricanes also occur outside of that period.

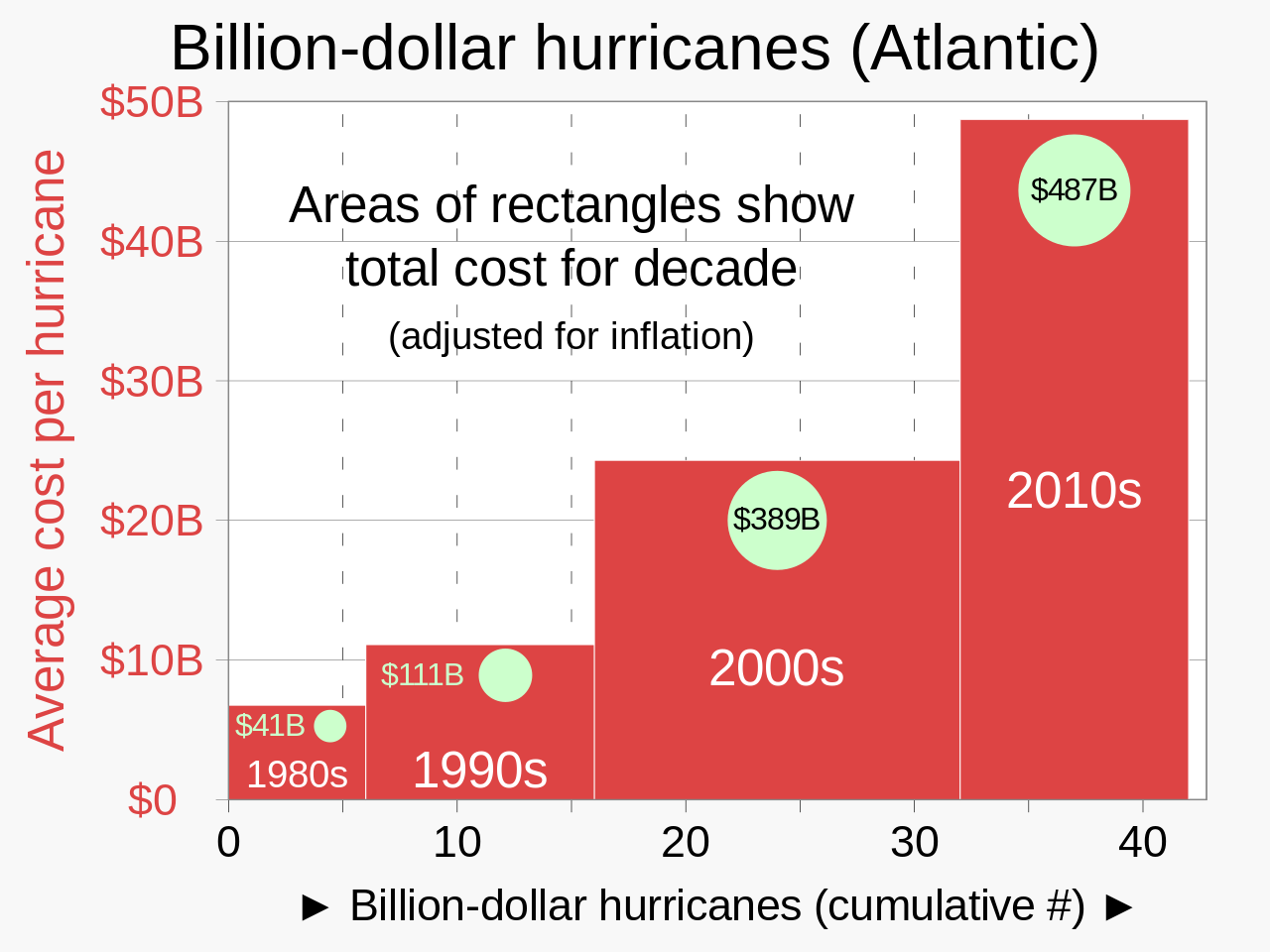

Not only are the chances of a major hurricane occurring each year increasing, but so are their costs.

The number of $1 billion Atlantic hurricanes nearly doubled from the 1980s to the 2010s, and their inflation-adjusted costs rose more than 11 times. This increase is believed to be due to climate change and increasing population to coastal areas. sauce: Wikipedia

But you knew that, right? We all know that global warming is accelerating, and that the chances of avoiding frequent and large-scale disasters are decreasing year by year.

Insurance costs are already rising

The cost of insuring a home or business, or livelihood, naturally increases as the probability of a disaster increases, and at some point the insurance runs out.

So how safe are we living in a dangerous state? Bloomberg Green I looked at it Insurance states by state:

U.S. home insurance premiums could set record this year, report warns

The average premium for homeowners insurance in the U.S. this year is expected to reach $2,522, a 6% increase from the end of 2023. Insurance premiums in Florida will be closer to $12,000.

Not a good headline. The article continues as follows (emphasis mine):

In the 1980s, the country was approx. Three disasters a year cause at least $1 billion in damage Each. In the 2010s, Increased to 13 cases per year, according to the National Oceanic and Atmospheric Administration.Last year, the US endured A record 28 weather disasters that caused at least $1 billion in damage each.

More and more insurance companies are withdrawing from the insurance industry in response to the threat posed by climate change. California and florida, where its influence is often felt. To fill this gap, state-run “insurers of last resort” are absorbing trillions of dollars of risk.

„The highest-risk areas may become uninsurable,“ said Betsy Stella, Insurify's vice president of carrier management and operations.

For California, as the article points out, immigration has already begun.

Starting in July, State Farm General Insurance Co. will cut about 72,000 policies in California, the state's largest insurer said, as it combats increased risks from wildfires and other natural disasters. This is the latest measure.

The move comes just nine months after State Farm announced plans to stop issuing new insurance in the nation's most populous state. …

State Farm cited the company's financial health as the reason for the layoffs. As disasters accumulate, insurance companies in other states are expected to reach the same conclusion.

Regarding Florida, Bloomberg says: “Florida homeowners already pay the highest home insurance premiums in the nation, and this year they are expected to see an additional 7% increase, bringing the state average to $11,759, more than four times the national average. .”

Anecdotally, a woman I know in Florida said her homeowner's insurance went from $3,000 to $14,000 in just six years. It should be obvious where this ends.

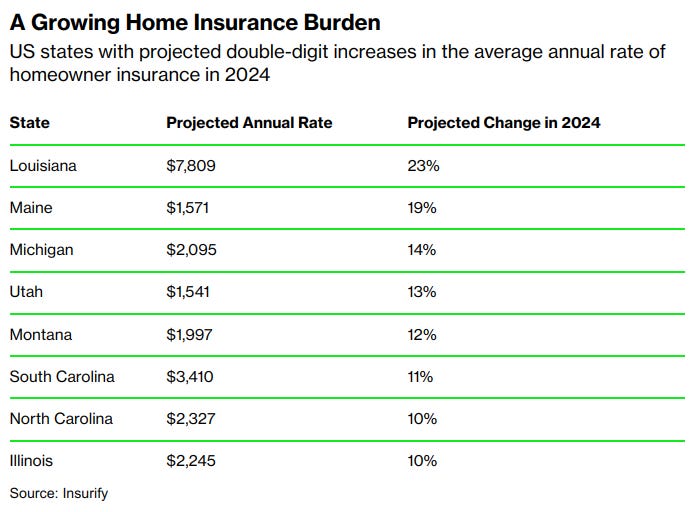

It's not just Florida

Homeowners insurance rates will increase by double digits in seven states, excluding Florida.

Bloomberg says:

In states where insurance premiums are rising, Insurify researchers primarily point to an increase in natural disasters. According to AccuWeather, 'Explosive' hurricane season expected in US This year, up to 25 named storms are possible between June and November, with an average of about 14. Meanwhile, sea-level rise and other negative climate impacts are catching up with historically low-risk states like Maine.

What else can you expect?

Is it time to consider a change?

The good news is that even in a state where bad things happen, the worst is yet to come. You have time to leave before everyone else leaves first, but you end up being left at the sales floor with no one who wants to buy.

The bad news is clear. For many people, a world without insurance is on the horizon. Numbers vary, but according to NOAA: 40% of Americans live in coastal counties.

NOAA estimates that U.S. coastal counties would rank third in global GDP if they were their own. All of this will sooner or later be lost due to sudden disasters and, ultimately, rising sea levels.We can expect insurance companies to exit those areas first the status of those liabilities incurred;

A world without insurance. Can I start planning now?