alphabet (NASDAQ:GOOG) (NASDAQ:Google) had more than $110 billion in cash and cash equivalents on its balance sheet at the end of 2023. The company is investing heavily in artificial intelligence, with capital spending expected to rise 27% this year from a record $32 billion last year. Bloomberg.

But several Wall Street analysts saw the pile of cash as evidence that Alphabet was preparing to pay a dividend. Lo and behold, when the company reported its first quarter results last week, management announced that it would pay a dividend of $0.20 per share on June 17th to shareholders of record on June 10th.

This makes Alphabet the world's newest dividend stock. Nasdaq 100an index that tracks the world's 100 largest companies. Nasdaq Stock Exchange. But investors shouldn't interpret this news to mean Alphabet lacks growth prospects. On the contrary, the company's market capitalization could reach $4 trillion by 2030, suggesting it has 90% upside potential.

Here's what investors need to know.

Alphabet looked strong in the first quarter

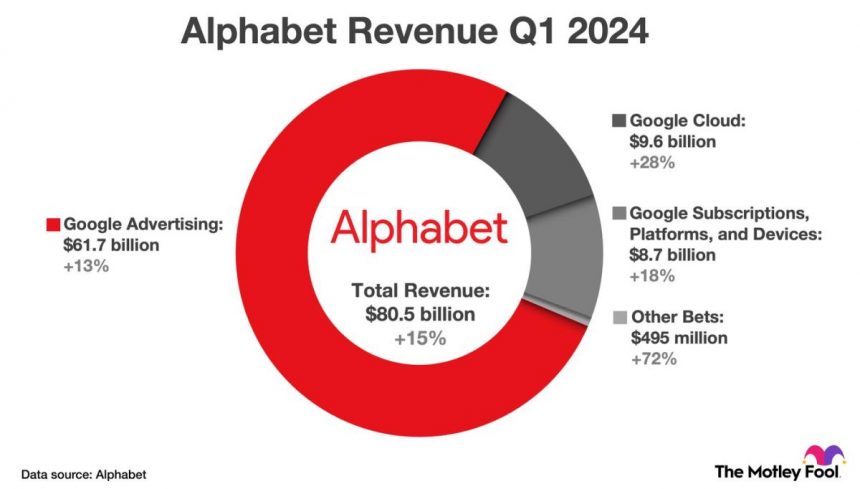

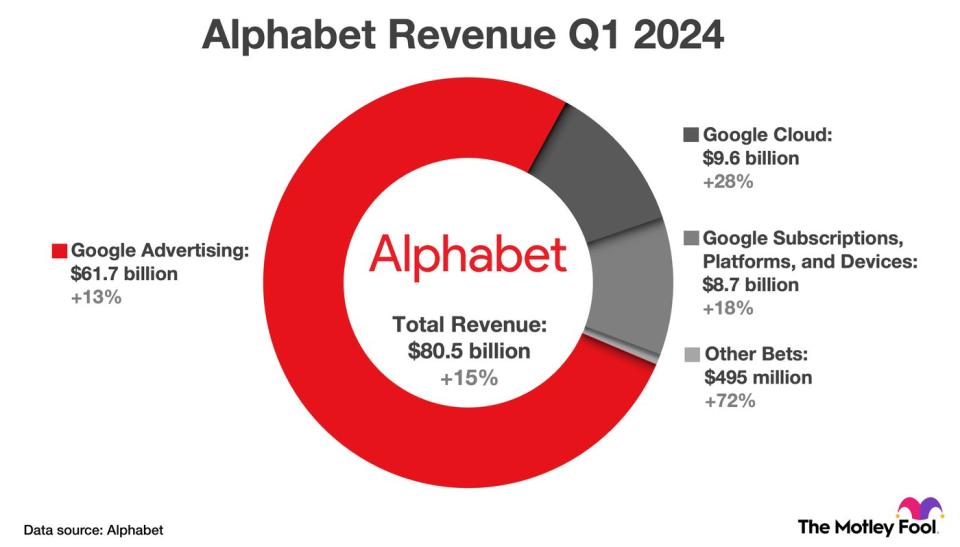

Alphabet reported impressive financial results in the first quarter, easily beating Wall Street expectations in terms of revenue and bottom line. Revenue rose 15% to $80.5 billion, with particularly strong momentum in Google Cloud, a product category that includes cloud infrastructure and platform services, and a business productivity suite called Google Workspace.

Alphabet has worked to optimize its cost base by focusing on the most attractive product development opportunities and right-sizing its workforce. This strategy continued to pay off in the first quarter. Operating margin expanded 700 basis points (7 percentage points); GAAP Net income increased 62% to $1.89 per diluted share.

The chart below details Alphabet's first quarter revenue growth across its four major product categories.

Looking ahead, management sees significant growth opportunities in search advertising and cloud computing, particularly in areas related to artificial intelligence (AI). CEO Sundar Pichai said, „Our leadership in AI research and infrastructure, as well as our global product footprint, positions us well for the next wave of AI innovation.“

In terms of the company's footprint, Alphabet has six products that serve more than 2 billion monthly users, including Google Search, YouTube, Chrome, and Android. This gives the company deep insight into consumer tastes and preferences, and that data can inform the company's machine learning models to improve campaign outcomes for media buyers. Additionally, Gemini, Alphabet's latest generative AI model, allows advertisers to build campaigns using natural language prompts and create relevant media assets (images and text).

Beyond advertising, Alphabet's Gemini model allows developers to build generative AI applications on Google Cloud and automate tasks across Google Workspace applications. For example, Gemini can draft text in Google Docs, create media content in Google Slides, and organize data in Google Sheets.

Alphabet has growth opportunities in digital advertising and cloud computing

Alphabet has two key growth engines: digital advertising and cloud computing. Although the company is expected to lose share across the broader advertising market in the coming years, it will still account for about 27% of digital ad spending in 2025, about 490 basis points more than its closest competitor. . meta platformaccording to eMarketer.

In particular, Alphabet continues to have an advantage in search and video advertising. Google dominates internet searches with over 91% of its market share, and YouTube is the most popular streaming service when measured by viewing time. In particular, some investors have expressed concerns that generative AI could erode Google's search dominance, and Alphabet is leaning into that trend with Search Generative Experience (SGE).

SGE applies generative AI to Google Search to help users understand topics faster and more deeply, while prioritizing traffic to websites and merchants. Mr. Pichai provided an update on the latest financial results. “We are seeing an increase in search usage among people using the new AI overview, and user satisfaction with the results is also increasing,” he said.

In cloud computing, Alphabet's Google Cloud Platform (GCP) is not that big. Amazon Web services are also not gaining market share as quickly as Web services. microsoft Azure. However, in recent years he GCP has become popular. It accounted for 11% of cloud infrastructure and platform services spending in Q4 2023, up 1 percentage point from 2021 and 3 percentage points from 2019.

Going forward, GCP is likely to continue gaining market share in the cloud as Gemini and other AI products gain adoption. In fact, Pichai hinted at that possibility in his latest earnings call. „We have the best infrastructure for the AI era,“ he said. “More than 60% of the funded generative AI startups and almost 90% of the generative AI unicorns are Google Cloud customers.”

Why Alphabet can become a $4 trillion company by 2030

Wall Street expects Alphabet to grow revenue by 10.5% annually over the next five years. I think there is room for upside, especially if Alphabet continues to gain market share in cloud computing. I say that because the online advertising and cloud computing markets are projected to grow at 16% and 14% annually through 2030, respectively.

This would give Alphabet 12% annual sales growth through the end of the decade. At this pace, sales in the next 12 months would reach $628 billion in six years, and if the stock traded at 6.4 times sales, the company would have a market cap of $4 trillion. This is a discount of the current valuation of 7.2 times sales, which is roughly in line with the average of the past three years of 6.3 times sales.

If Alphabet's market cap reaches $4 trillion in six years, that would represent a 90% upside for investors, or an 11.3% annual return. That makes this Magnificent Seven stock an attractive long-term investment idea.

Should you invest $1,000 in Alphabet right now?

Before buying Alphabet stock, consider the following:

of Motley Fool Stock Advisor Our analyst team has identified what they believe Best 10 stocks Investors can buy now…and Alphabet wasn't one of them. These 10 stocks have the potential to generate impressive returns over the next few years.

when to think about it Nvidia This list was created on April 15, 2005…if you invested $1,000 at the time of recommendation. you have $537,557!*

stock advisor provides investors with an easy-to-understand blueprint for success, including guidance on portfolio construction, regular updates from analysts, and two new stocks each month.of stock advisor For the service more than 4 times The resurgence of the S&P 500 since 2002*.

*Stock Advisor will return as of April 22, 2024

Randi Zuckerberg is a former head of market development and spokesperson at Facebook, sister of Meta Platforms CEO Mark Zuckerberg, and a member of the Motley Fool's board of directors. Suzanne Frey, an Alphabet executive, is a member of the Motley Fool's board of directors. John Mackey, former CEO of Amazon subsidiary Whole Foods Market, is a member of the Motley Fool's board of directors. Trevor Jennewine I have a position on Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: A long January 2026 $395 call on Microsoft and a short January 2026 $405 call on Microsoft. The Motley Fool has Disclosure policy.

Introducing the latest dividend stocks from the Nasdaq 100. With the help of artificial intelligence, it could become a $4 trillion company by 2030. Originally published by The Motley Fool